The Engineering Software Apocalypse Was Inevitable

Six months of evidence on the question every infrastructure PM is half-asking: are we watching engineering software disappear into AI agents? Short read: not disappearing. Becoming a piece. The accountability moat says why.

What I have been watching

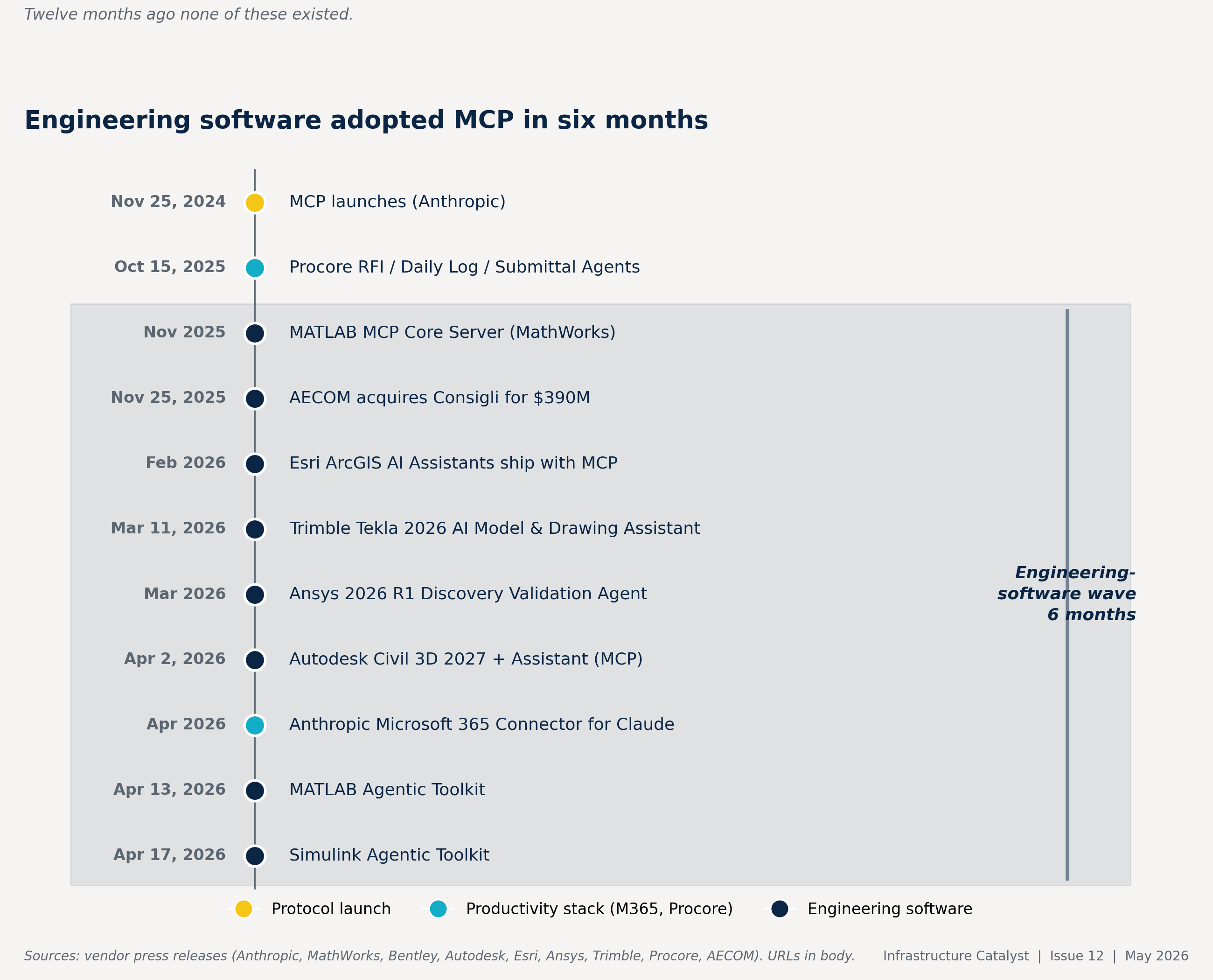

Every major AEC software vendor shipped an MCP server in the last six months. None of them are defending their position. They are signing it away on purpose.

I spent the first half of 2026 reading AI policies, testing frontier models on engineering tasks, and tracking what every major AEC software vendor shipped. The question I keep coming back to is whether engineering specialized software, the Civil 3D and Bluebeam and MATLAB and ArcGIS that infrastructure PMs rely on every week, is being absorbed by AI agents that drive it from the outside.

The short read after six months of evidence: not absorbed. Restructured. Becoming a piece. For the next few years, the agent layer calls into the engineering software, and the engineering software keeps doing what it has always done. The seat license is the part that looks fragile. The system of record, the audit trail, the named software in a contract clause, the file format the PE seals are not fragile. They are getting more important.

This issue lays out what I have seen and where the question lands as of May 2026.

The architecture has already been signed away

The Model Context Protocol launched in November 2024. By December 2025, Anthropic donated MCP to the Linux Foundation. Between November 2025 and April 2026, every major AEC software vendor shipped an MCP server.

The roster:

- MathWorks released the MATLAB Agentic Toolkit on April 13, 2026 and the Simulink Agentic Toolkit on April 17.

- Bentley shipped an MCP server for STAAD.

- Autodesk Civil 3D 2027 ships the Autodesk Assistant with MCP.

- Esri added MCP-backed AI assistants in ArcGIS in February 2026.

- Ansys 2026 R1 shipped the Discovery Validation Agent in March 2026.

- Trimble Tekla 2026 added the AI Model and Drawing Assistant on March 11, 2026.

- Bluebeam Max ships Claude integration via MCP plus AI-MATCH from the Firmus AI acquisition (September 2025).

Eleven shipped products in eighteen months. The engineering wave is the last six. The vendors are not defending their position. They are co-authoring the protocol that lets agents drive their software directly. Twelve months ago none of this existed.

What the executives are saying

Tech splits cleanly on the same question. Microsoft CEO Satya Nadella on the BG2 podcast (December 2024) frames business applications as collapsing into AI agents that own the business logic. Autodesk CEO Andrew Anagnost at Autodesk University 2025 said neural CAD will automate 80 to 90 percent of routine design tasks. Marc Benioff coined "SaaSpocalypse" on Salesforce's Q4 FY26 earnings call (February 25, 2026) but argued against it: the system of record persists, foundation models commoditize underneath. Ben Thompson at Stratechery (Microsoft and Software Survival, 2026) holds the same line: the application boundary is the moat and agents inherit it.

Both sides are credible. The question for an infrastructure PM is which read holds for engineering software specifically, in the next two to three years.

What the data is saying

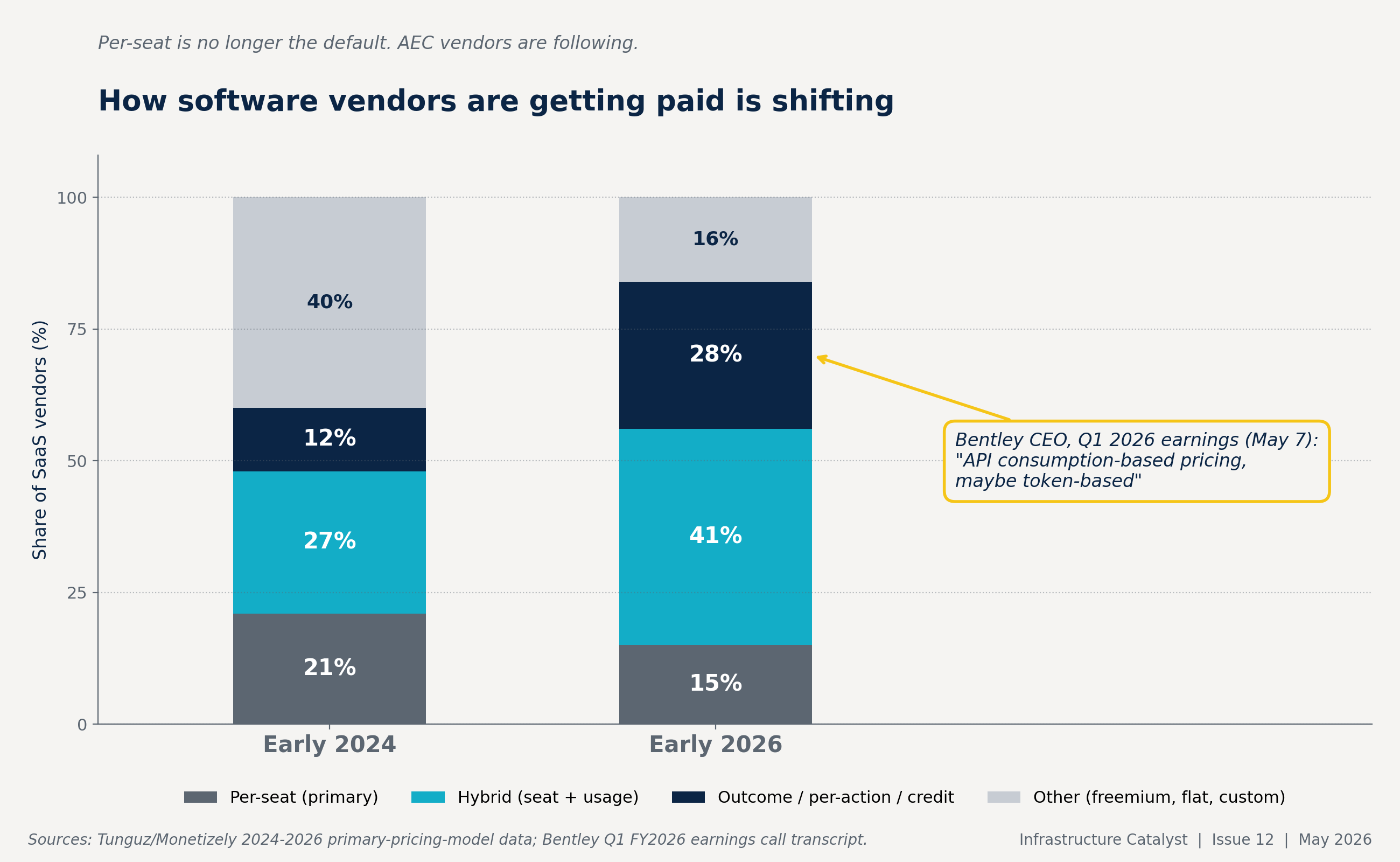

The market repriced software through 2025. The software sector lost roughly $2 trillion in market cap year to date; the iShares software ETF (IGV) tracked the decline. Forward P/E for software compressed from 84x at the 2020-2022 peak to 22.7x in Q1 2026. For the first time ever, software trades at a discount to the S&P 500 (Bain, February 2026; SaaStr, March 2026).

Pricing is the cleaner empirical signal. Salesforce launched Agentforce Flex Credits at $0.10 per action in May 2025. Sierra AI hit $150 million in ARR by early 2026 charging only on successful resolution. Tomasz Tunguz tracked seat-based pricing dropping from 21% of vendors to 15% in twelve months while hybrid pricing surged from 27% to 41%.

For AEC specifically, Bentley CEO Nicholas Cumins named the destination on the Q1 FY2026 earnings call (May 7, 2026):

"For the engineering applications, we'll be in API consumption-based pricing, maybe token-based because that seems to be the common denominator across different AI tools."

That is the first AEC vendor to put the per-API-call shift on tape on an earnings call.

The customer side is moving too. I covered AECOM's $390 million acquisition of Consigli, a Norwegian AI engineering startup, in Issue #2 back in December. Memoori, the AEC technology research firm, called it an inversion of normal AEC M&A direction.

Six months later, here is where it has gone. On AECOM's Q1 FY26 earnings call (February 10, 2026), CEO Troy Rudd said the firm had "completed the integration of our September acquisition" and "doubled the size of our [AI] team." On the Q2 FY26 call (May 12, 2026), Rudd named two contract wins totaling "almost a billion dollars" where AECOM's "proprietary AI solution" was "a central element." CFO Gaurav Kapoor pegged Q2 AI spend at $13 million, about 66 basis points of margin.

The detail I keep coming back to: across two earnings calls and an April Southern Methodist University doctoral fellowship announcement, AECOM has stopped saying the name "Consigli." Janne Aas-Jakobsen, the Consigli founder who became AECOM's Head of AI Engineering, appears in the SMU release without a Consigli reference. The brand is being absorbed into "proprietary AI." The vendor name disappears. The agent layer survives. The accountability sits with the firm that won the billion-dollar contract.

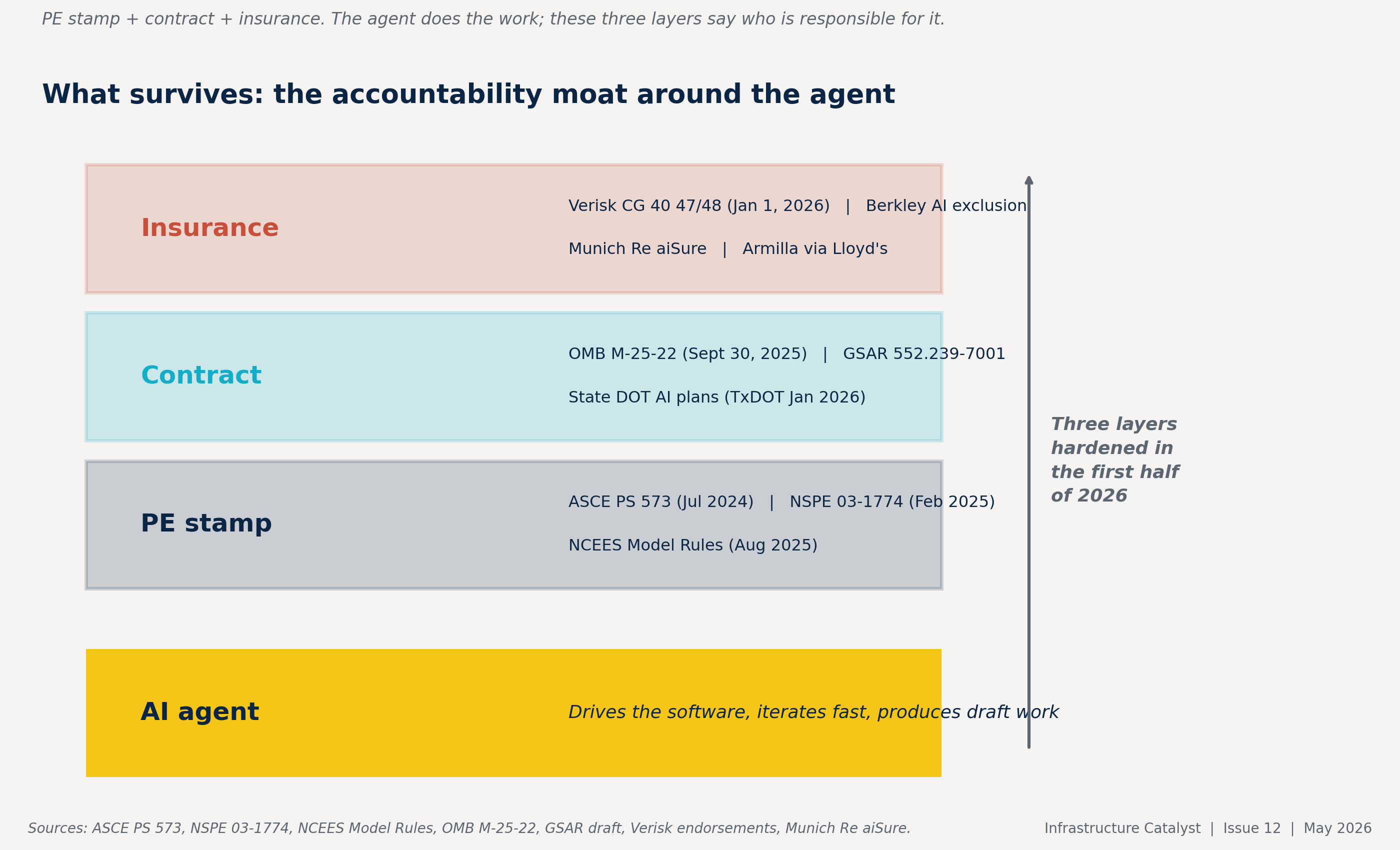

What survives: the accountability moat

The thing the absorption thesis usually misses is what is happening in parallel with the agent buildout: the accountability framework around engineering deliverables is hardening, not loosening.

Three layers tightened in the first half of 2026.

The PE stamp. ASCE Policy Statement 573 (July 2024) holds that "AI cannot serve as a replacement for the professional judgement of a licensed Professional Engineer." NSPE Position Statement 03-1774 (revised February 2025) requires those who design, develop, or oversee AI systems with public-safety impact to be held to the same licensure standard as traditional engineers. The NSPE Board of Ethical Review ruled in Fall 2025 that misuse of AI without Responsible Charge is unethical. NCEES Model Rules (August 2025) define Responsible Charge as direct control and personal supervision; the definition has not been softened to accommodate AI.

The contract. OMB Memorandum M-25-22 (effective September 30, 2025) requires federal AI contracts to include monitoring, performance evaluation, and vendor reassessment. GSAR 552.239-7001 (draft March 6, 2026) requires contractors to submit a current model provenance statement naming the developer, third-party model sources, and training data categories. TxDOT's AI Strategic Plan (January 2026) reinforces a human-led, AI-supported governance philosophy and flows down to consultants on TxDOT contracts.

The insurance. Verisk released two standardized GenAI exclusion endorsements (forms CG 40 47 and CG 40 48) effective January 1, 2026. Berkley filed an absolute AI exclusion endorsement for D&O, E&O, and Fiduciary Liability policies. AIG and Great American filed similar. Stanford Law data cited in the carrier filings: general-purpose AI tools produce inaccurate outputs between 58% and 88% of the time. Affirmative AI E&O coverage exists from Munich Re (aiSure) and Armilla Insurance Services via Lloyd's, with limits from $2 million to $50 million.

NIST published the concept note for the AI Risk Management Framework Critical Infrastructure Profile on April 7, 2026. It calls for "AI bills of materials to provide traceable, auditable rationales for recommendations." That phrase is going to matter. Within eighteen months, the deliverable an agent helped produce will need to be paired with an AI BoM the way structural calculations have always been paired with a stamped calc set.

What lands on your desk first

Put the architecture, the data, the contract floor, and the accountability moat together and the picture is not "engineering software is dying." It is "engineering software is becoming the integration layer the agent calls into, the contract names, and the insurer underwrites."

The PM-coded version: the staff engineer doing rote software operation is the role most at risk. The PM running the agent stack and the PE defending the deliverable are the roles most upgraded. PMBOK 8 (November 13, 2025) and the PMP exam refresh (July 1, 2026) have already repositioned the PM role around AI orchestration. PMI is naming what is about to happen.

For the firm, the first concrete thing that lands is the insurance renewal. By the next E&O cycle, your broker will hand you an AI questionnaire. Firms with four pieces in place will renew on standard terms:

- A written AI use policy

- Agent and prompt logging

- PE sign-off workflows on AI-assisted deliverables

- Munich Re (aiSure) or Armilla affirmative AI E&O coverage

Firms without those four will pay surcharges, accept exclusions, or both. The AI questionnaire is the moment the apocalypse shows up on a CFO's line item.

Three questions I am still watching

The eighteen-month picture is clearer than the five-year picture. Three things will move the call.

How far the tool plugins evolve. If MCP becomes the universal driver and Claude or GPT-5 or Gemini can invoke any engineering software with low friction, the GUI moat erodes faster than I expect. If MCP stays partial and most workflows still need someone in the application, the seat license persists longer than the doomsayers think.

How fast the foundation models keep improving. If model error rates fall from the 58 to 88% general baseline (today's Stanford Law data) to 5 to 10% on engineering tasks within two years, the pressure on insurers and PE boards to update their position increases sharply. If model error rates stay roughly where they are, the accountability moat holds and the agent layer stays a tool the PE supervises.

Which platform wins the orchestration layer. If Microsoft (M365 Connector for Claude, the Copilot stack, Azure) dominates, infrastructure firms standardized on Microsoft adopt fast. If Google or OpenAI takes the orchestration layer, a different adoption curve. If the orchestration layer fragments by vertical (Bluebeam owns drawings, MATLAB owns simulation, Procore owns construction operations), then "engineering software is becoming a piece" stays true longer than three years.

And a question I am starting to dig into for a future issue: financial private equity is rolling up specialty trades aggressively, and what they want from AI looks structurally different from what engineering consulting firms want. The moat for the trades roll-up is operational standardization; the moat for the consulting firm is the PE stamp. If you know which named PE platforms in AEC are actually paying for this work, reply.

I do not have answers to those questions. Anyone telling you they do is selling something.

Joseph Dib, PE, PMP

Infrastructure Catalyst